I have been riding my make-shift stationary recumbent exercise bike for about 80 minutes so far and it is giving me a great workout. However, riding a stationary bike is quite boring. It would be a great idea for someone to invent a virtual reality bike that allows me play a racing game and control the tank, bike, or car with my bike. It would be even better if you could change scenery (or levels), make your own scenery, or even race against other people.

It would be good if such an invention could allow you to simply plug your bike into a spare TV.

Update: It seems as if someone has already come up with this idea. See Virtual Bike Improves Safety. What I had in mind though is a cheap, mass-produced recumbent bike that can easily be plugged into the TV. The software will already be in the bike's computer. The virtual bike in the BBC article is for a motorbike and the equipment looks very expensive. Given that obesity is set to rise in the future at a rapid rate, such an invention I'm sure will be very popular.

26 October 2008

25 October 2008

The Genki 18kg Flywheel Fitness Gym Exercise Bike

I used to have an elliptical trainer than I used for exercise. It served me well but there were a few problems with it. Firstly, the elliptical trainer only let me stand. When I am exercising for a long period of time, I have to stand up for a long period of time, which meant that my ankles got sore. After some weeks of intense usage, I broke the machine beyond repair.

So I purchased the Genki 18kg Flywheel Fitness Gym Exercise Bike from Crazy Sales. I was pleased because the bike only cost me about $250 including delivery. The bike was delivered very quickly (about 3 days). The package is 48 kilograms, so be careful because it is incredibly heavy.

My parents set up the bike for me. I think this exercise bike is great, but I have noticed some problems. The first problem is that the pedals have sharp metal spikes on them, which means that you really cannot use the bike barefoot. This is a minor problem because I can easily put on some shoes.

The major problem with this bike is the seat, which is small and hard. I only had to be on the bike for 10 minutes before my bum got sore. It is absolutely intolerable! I am going to have to look for a bicycle seat that I can use to replace the seat given.

I have been looking at Ergo the Seat and what they say really is scary. They claim that bad bike seats can constrict nerves and cause impotence! What a way to make people buy your product.

Update: I have solved the problem. I was thinking of buying a new recumbant bicycle but didn't want to spend another $200 on it. Instead, I will just put a normal chair directly behind my exercise bike, sit on this chair, and then pedal like normal. For more comfort I can put a pillow on the chair. In other words, I use the upright bike as if it were a recumbent bicycle.

So I purchased the Genki 18kg Flywheel Fitness Gym Exercise Bike from Crazy Sales. I was pleased because the bike only cost me about $250 including delivery. The bike was delivered very quickly (about 3 days). The package is 48 kilograms, so be careful because it is incredibly heavy.

My parents set up the bike for me. I think this exercise bike is great, but I have noticed some problems. The first problem is that the pedals have sharp metal spikes on them, which means that you really cannot use the bike barefoot. This is a minor problem because I can easily put on some shoes.

The major problem with this bike is the seat, which is small and hard. I only had to be on the bike for 10 minutes before my bum got sore. It is absolutely intolerable! I am going to have to look for a bicycle seat that I can use to replace the seat given.

I have been looking at Ergo the Seat and what they say really is scary. They claim that bad bike seats can constrict nerves and cause impotence! What a way to make people buy your product.

Update: I have solved the problem. I was thinking of buying a new recumbant bicycle but didn't want to spend another $200 on it. Instead, I will just put a normal chair directly behind my exercise bike, sit on this chair, and then pedal like normal. For more comfort I can put a pillow on the chair. In other words, I use the upright bike as if it were a recumbent bicycle.

Property a Safe Haven from Volatile Shares?

Some people are saying that dropping share markets in Australia will see most investors putt their money into property, which is allegedly safer. The Rudd Government has also increased the First Home Owners Grant (FHOG), which makes it tempting for some people to buy property.

However, I will argue that the share market and the property market do not exist independently. One affects the other.

When the recession hits, Aussie businesses will not longer require as many immigrants, which will reduce the numbers coming here, which will reduce demand for houses, which will reduce house prices.

As unemployment increases, people will have less money to buy houses, which means demand decreases, decreasing prices of houses. Many of those workers laid off will not be able to pay off mortgages, meaning they will be forced to sell, meaning more houses flood the market, which decreases prices.

I have been looking at the economic analyses of economists Steve Keen at UNSW and Robert Shiller at Yale University. They show that real house prices in all countries over many centuries are constant at approximately 3 times average yearly income. Australia currently has the most expensive houses in the world at 7 or 8 times annual income. We are in the same position as California was before property crashed there, causing house prices to decline 40% in one year.

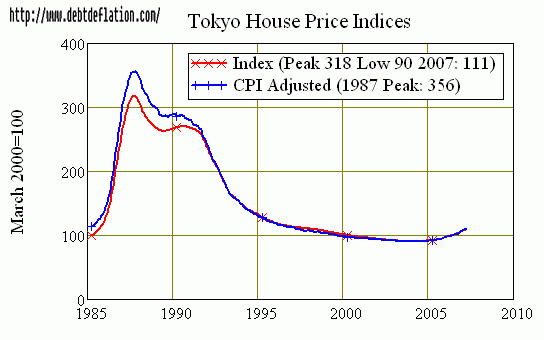

Some people say that property increases in the long term. They say that it may be the case that American house prices are going down, but in the future it will increase again. This may be true, but consider that historically property prices stagnate for long periods of time. Take house prices in Tokyo. After the 1990 Banking Crisis in Japan, property prices in Tokyo plunged by 70 per cent from then (1990) till today (2008). This means that in 18 years property prices have gone down by 70 per cent. Who knows how many more decades it will take before Tokyo property prices go back up to the levels it reached in 1990?

Related Podcast: The Property Bubble (Counterpoint)

However, I will argue that the share market and the property market do not exist independently. One affects the other.

When the recession hits, Aussie businesses will not longer require as many immigrants, which will reduce the numbers coming here, which will reduce demand for houses, which will reduce house prices.

As unemployment increases, people will have less money to buy houses, which means demand decreases, decreasing prices of houses. Many of those workers laid off will not be able to pay off mortgages, meaning they will be forced to sell, meaning more houses flood the market, which decreases prices.

I have been looking at the economic analyses of economists Steve Keen at UNSW and Robert Shiller at Yale University. They show that real house prices in all countries over many centuries are constant at approximately 3 times average yearly income. Australia currently has the most expensive houses in the world at 7 or 8 times annual income. We are in the same position as California was before property crashed there, causing house prices to decline 40% in one year.

Some people say that property increases in the long term. They say that it may be the case that American house prices are going down, but in the future it will increase again. This may be true, but consider that historically property prices stagnate for long periods of time. Take house prices in Tokyo. After the 1990 Banking Crisis in Japan, property prices in Tokyo plunged by 70 per cent from then (1990) till today (2008). This means that in 18 years property prices have gone down by 70 per cent. Who knows how many more decades it will take before Tokyo property prices go back up to the levels it reached in 1990?

{kind=link}

Related Podcast: The Property Bubble (Counterpoint)

22 October 2008

Don't Classify Necessities Using Simplistic Categories

I have noticed that losing weight and being biologically healthy is very similar to being financially healthy. When you want to lose weight, you must burn off more calories than you consume. When you want to be financially healthy, you must spend less than you earn. Is it then not surprising that Americans and Australians are both obese and indebted. I believe that the behavioral make-up of those likely to be obese makes them likely to have huge debt. In fact, debt can be seen as a form of obesity.

When you want to be thrifty, you need to identify the difference between needs and wants. Needs are those things that you really need for physiological survival, e.g. food, water, a bed, a roof over your head, etc. Wants are things like luxury cars and plasma TVs. The problem is that the distinction between wants and needs is not clear-cut. One person's want is another person's need. For example, a drug addict really needs drugs because he or she is dependent on it. For someone who is not addicted to that drug, it is not so important.

One solution to this problem I use is to make money hard to get. For example, take a box, put $500 in it, then buy 10 small padlocks and lock the box up. Then hide the keys all around the house. If you want to spend that $500, you have to put in a lot of effort to go around the house, find the keys, and unlock the box. The difficulty of getting this money I believe will ensure that you will only go through the effort of opening the box if what you want the money for really is a necessity.

The reason why I started this post was to warn people against classifying necessities using simplistic categories. What I mean by this is thinking that, say, food is a necessity. Food may be a necessity, but that does mean that certain types of food are not wants. For example, eating bran cereal (which is high in fiber) for breakfast I think is a necessity. However, eating a $1000 meal at an upscale restaurant is a want, not a necessity. Someone who goes around thinking that food is a necessity will likely use this to rationalize buying luxury food.

When you want to be thrifty, you need to identify the difference between needs and wants. Needs are those things that you really need for physiological survival, e.g. food, water, a bed, a roof over your head, etc. Wants are things like luxury cars and plasma TVs. The problem is that the distinction between wants and needs is not clear-cut. One person's want is another person's need. For example, a drug addict really needs drugs because he or she is dependent on it. For someone who is not addicted to that drug, it is not so important.

One solution to this problem I use is to make money hard to get. For example, take a box, put $500 in it, then buy 10 small padlocks and lock the box up. Then hide the keys all around the house. If you want to spend that $500, you have to put in a lot of effort to go around the house, find the keys, and unlock the box. The difficulty of getting this money I believe will ensure that you will only go through the effort of opening the box if what you want the money for really is a necessity.

The reason why I started this post was to warn people against classifying necessities using simplistic categories. What I mean by this is thinking that, say, food is a necessity. Food may be a necessity, but that does mean that certain types of food are not wants. For example, eating bran cereal (which is high in fiber) for breakfast I think is a necessity. However, eating a $1000 meal at an upscale restaurant is a want, not a necessity. Someone who goes around thinking that food is a necessity will likely use this to rationalize buying luxury food.

19 October 2008

Is It a Good Time to Buy?

After global markets have been battered, investor Warren Buffett is telling everyone to buy. The argument is that the panic selling was irrational and because of irrational selling the market is undervalued. The companies themselves are sound but the price has been discounted too far.

However, is this true? If the gloomy news about lower profits and credit freezes are true, then companies may not be fundamentally sound. One measure of a company is the price-earnings ratio, a measure of whether a company's stock is overvalued or undervalued. The problem with the PE ratio is that past earnings are used to calculate this ratio. In the past earnings may have been great because our economy was booming. However, with the credit freeze and looming recession, who is to say earnings won't go down? Maybe the market is rational if it reduces price in line with what is expected to be a reduction in earnings.

Nevertheless, I was looking at Wikipedia today and Robert Shiller has created a nice scatterplot showing how investing in companies with PE ratios of 10 or below gave the best returns.

In my opinion, the inherent value in shares comes from its dividends since earnings reports can be fudged by unethical accountants. The long run average price-dividend ratio for the S&P500 is 24.

This empirical evidence suggests that a contrarian investment strategy (similar to what Buffett suggests) is best. You go all-in to stocks when the market has low PE or PD ratios and you hold back (set aside more in cash) when the market has high PE or PD ratios. Of course, if everyone sees this opportunity to profit and employs this contrarian strategy, then the contrarians will become mainstream and then being contrary won't be contrarian anymore. I was talking with some friends before and one of them said, "Now is a great buying opportunity because stocks are do cheap. You should buy when everyone else is selling." However, another friend, a successful full-time day trader, replied by saying, "I am selling now because I am contrarian. There are plenty of irrational buyers still out there that I want to exploit." So as you can see, while there may be plenty of bulls who look for opportunities to buy low to exploit irrational sellers, inversely there are many bears who look for opportunities to sell high to exploit irrational buyers.

However, is this true? If the gloomy news about lower profits and credit freezes are true, then companies may not be fundamentally sound. One measure of a company is the price-earnings ratio, a measure of whether a company's stock is overvalued or undervalued. The problem with the PE ratio is that past earnings are used to calculate this ratio. In the past earnings may have been great because our economy was booming. However, with the credit freeze and looming recession, who is to say earnings won't go down? Maybe the market is rational if it reduces price in line with what is expected to be a reduction in earnings.

Nevertheless, I was looking at Wikipedia today and Robert Shiller has created a nice scatterplot showing how investing in companies with PE ratios of 10 or below gave the best returns.

In my opinion, the inherent value in shares comes from its dividends since earnings reports can be fudged by unethical accountants. The long run average price-dividend ratio for the S&P500 is 24.

This empirical evidence suggests that a contrarian investment strategy (similar to what Buffett suggests) is best. You go all-in to stocks when the market has low PE or PD ratios and you hold back (set aside more in cash) when the market has high PE or PD ratios. Of course, if everyone sees this opportunity to profit and employs this contrarian strategy, then the contrarians will become mainstream and then being contrary won't be contrarian anymore. I was talking with some friends before and one of them said, "Now is a great buying opportunity because stocks are do cheap. You should buy when everyone else is selling." However, another friend, a successful full-time day trader, replied by saying, "I am selling now because I am contrarian. There are plenty of irrational buyers still out there that I want to exploit." So as you can see, while there may be plenty of bulls who look for opportunities to buy low to exploit irrational sellers, inversely there are many bears who look for opportunities to sell high to exploit irrational buyers.

10 October 2008

Bad Omen Precedes a Massive Stockmarket Crash

Last night when I was driving back from work I swerved to missed a dead cat on the road. The cat looked intact except for its behind, which was probably run over by tires. There was a pool of blood next to the cat. The thought that maybe this cat was still alive and suffered from excruciating pain made me feel horrible. Parents who do not watch their children can be charged with child abuse, so I don't know why so many cat owners do not watch their cats. Many seem happy to just let them run around on the streets.

When I woke up today and checked the news, I realized that the Australian stock market had tanked. The All Ords had fallen by about 8 per cent to 3900. All up I've probably lost about $8000 or $9000 now. I am thankful that I am still relatively young and have little invested in the stock market. Losing $8000 may seem painful but I have heard about older retirees losing $400,000. I suppose I can be thankful that this depression happened while I was young rather than it building up and hurting me even more when I'm older and have even more money in the market. I am hoping this depression scares the highly-leveraged permabulls away from the market so we can start again with a clean slate from the bottom.

I am tired of all the people saying that now is a good buying opportunity because prices have gone down so much. They were saying this when the market dropped to 5000. They were saying this when the market dropped to 4500. They are still saying it when the market dropped to 3900. I think these people have the gambler's desire to win back losses. I like to use the analogy of the car. Sure, a 50 per cent price reduction in a car seems like a good discount, but just because the price has gone down it may not be a good time to buy. What if the engine in the car has just blown? I fear that the stock market decline may be a rational response to the economic equivalent of a blown engine. The engine that runs our economy (probably debt) is stuffed and now we are entering a phase of deleverage.

When I woke up today and checked the news, I realized that the Australian stock market had tanked. The All Ords had fallen by about 8 per cent to 3900. All up I've probably lost about $8000 or $9000 now. I am thankful that I am still relatively young and have little invested in the stock market. Losing $8000 may seem painful but I have heard about older retirees losing $400,000. I suppose I can be thankful that this depression happened while I was young rather than it building up and hurting me even more when I'm older and have even more money in the market. I am hoping this depression scares the highly-leveraged permabulls away from the market so we can start again with a clean slate from the bottom.

I am tired of all the people saying that now is a good buying opportunity because prices have gone down so much. They were saying this when the market dropped to 5000. They were saying this when the market dropped to 4500. They are still saying it when the market dropped to 3900. I think these people have the gambler's desire to win back losses. I like to use the analogy of the car. Sure, a 50 per cent price reduction in a car seems like a good discount, but just because the price has gone down it may not be a good time to buy. What if the engine in the car has just blown? I fear that the stock market decline may be a rational response to the economic equivalent of a blown engine. The engine that runs our economy (probably debt) is stuffed and now we are entering a phase of deleverage.

06 October 2008

Mutual Fund Indexing Not Good for Believers in EMH

I have been reading some sites and came across the following:

Source: How to Blend Index Funds

Here's my situation. I suspect that buying individual stocks yourself can be cheaper than investing in index mutual funds or ETFs because holding individual stocks doesn't eat up any management fees. You have to pay brokerage fees to buy the stocks, but you only pay once rather than annually, so that over the long run (30 or 40 years) your costs are virtually zero.

There are exception to the rule here. Many foreign, high-cost investments should be accessed using ETFs, such as emerging markets or frontier markets. However, if your discount online brokerage offers $20 trades to buy stock in domestic companies, I think that replicating the index yourself can save you money.

One problem is trying to constantly sell and buy once companies go off and on the index. This problem comes about because indexers set an arbitrary line between big and small companies. Many choose the S&P500. But why the top 500 companies? William Bernstein in The 15-Stock Diversification Myth claims the following: "Fifteen stocks is not enough. Thirty is not enough. Even 200 is not enough. The only way to truly minimize the risks of stock ownership is by owning the whole market." The whole market means the whole market, not the S&P500. It means everything, from small caps to large caps.

What I suggest then is using ETFs to cover the high-cost areas and for the low-cost areas, randomly sample from a population of all stocks using market cap as weight. Over time, as you buy, your cumulative sample will converge towards the market.

DIY (do-it-yourself) indexing will give you identical expected returns to an index mutual fund but because DIY indexing carries significantly lower costs, it follows that DIY indexing will beat index mutual fund investing over the long run in the same way that index mutual fund investing will beat active mutual fund investing in the long run (mainly because of fees).

Even if you are a die-hard believer in the efficient market hypothesis, that doesn’t mean you have to invest only in index funds. If the efficient market hypothesis is correct, then you won’t do any worse (on average) with a random collection of stocks within an index than you will by holding the index. If stock picking doesn’t matter, then you are free to pick any collection of stocks within the index that vaguely represents the index.

Some index funds perform poorly against the index not because they have high fees, but because they are trying to track the index too closely. When a stock is added to S&P 500, millions of dollars invested in S&P 500 Index funds must all buy that stock in order to track the index exactly. Stocks added to the S&P 500 do very poorly the year after this surge of automated buying. Funds that delay purchasing these stocks can perform better than those who purchase them immediately and pay a premium. Similarly, stocks that are being removed from the S&P 500 will out perform the index over the next year because all the index funds dumping the stock drive the price down needlessly. Delaying the sale of this stock until it has had a chance to recover produces superior returns.

Source: How to Blend Index Funds

Here's my situation. I suspect that buying individual stocks yourself can be cheaper than investing in index mutual funds or ETFs because holding individual stocks doesn't eat up any management fees. You have to pay brokerage fees to buy the stocks, but you only pay once rather than annually, so that over the long run (30 or 40 years) your costs are virtually zero.

There are exception to the rule here. Many foreign, high-cost investments should be accessed using ETFs, such as emerging markets or frontier markets. However, if your discount online brokerage offers $20 trades to buy stock in domestic companies, I think that replicating the index yourself can save you money.

One problem is trying to constantly sell and buy once companies go off and on the index. This problem comes about because indexers set an arbitrary line between big and small companies. Many choose the S&P500. But why the top 500 companies? William Bernstein in The 15-Stock Diversification Myth claims the following: "Fifteen stocks is not enough. Thirty is not enough. Even 200 is not enough. The only way to truly minimize the risks of stock ownership is by owning the whole market." The whole market means the whole market, not the S&P500. It means everything, from small caps to large caps.

What I suggest then is using ETFs to cover the high-cost areas and for the low-cost areas, randomly sample from a population of all stocks using market cap as weight. Over time, as you buy, your cumulative sample will converge towards the market.

DIY (do-it-yourself) indexing will give you identical expected returns to an index mutual fund but because DIY indexing carries significantly lower costs, it follows that DIY indexing will beat index mutual fund investing over the long run in the same way that index mutual fund investing will beat active mutual fund investing in the long run (mainly because of fees).

03 October 2008

Subprime Crisis and Japanese Banking Crisis

.svg)

I am starting to worry that the Subprime Crisis in America may play out similarly to the Japanese Banking Crisis. In Japan, property prices and stock prices were rising rapidly until about 1990 when both crashed. The Nikkei 225 has not recovered to this day, as you can see on the graph above, which I obtained from Wikipedia. What this teaches is that the future is uncertain and that stock markets don't necessarily go up in the long run. One could argue that in the future the Japanese stock market will recover, but 18 years of stagnation for me is sufficient evidence to disprove the assertion that stock markets always go up in the long run. It reminds me of what economist John Maynard Keynes said: "In the long run we are all dead."

Some argue that in America the S&P500 always goes up in the long run and historical data proves this. Indeed it does, but before 1990 we could say the same thing about the Nikkei 225. Who is to say that the credit crunch in America now won't produce the same stagnation for the next 10 to 20 years that we saw in Japan?

The Subprime Crisis and the Japanese Banking Crisis were both similar in that they were triggered by a stock market and property market bubble that popped and resulting in a drying up of liquidity as banks refused to lend. The response of regulators in both Japan and the US were similar in that they both tried to restore liquidity by lowering interest rates. Regardless of the regulators' intentions to prop up the banks, most were too scared to lend.

STW Versus ASX20

Many people buy STW on the Australian Stock Exchange if they want to buy an index fund that tracks the S&P/ASX 200. While on Ninemsn, I looked at the recent five-year performance of STW and then compared it to the performance of the ASX20 index. What I found was that there is a difference but the difference is quite small, and the ASX20 actually beats STW in this instance. This makes me wonder whether it's worth it to buy an index fund like STW and pay MER of 0.29% when I can easily build up a collection of 20 stocks that replicates the ASX20 using a broker like Commsec for a lot less. If I have a lot of money invested, even if I put half in an index fund and half in direct stocks that replicate an index, I am sure I can save a considerable amount in management fees and not have that much impact on investment performance.

01 October 2008

Net Worth Report for September 2008

Cash: $189

Kiva: $566

Vanguard Mutual Fund: $24442

Hesta Super Fund: $3336

Woodside Petroleum Shares: $1057

Car: $5825

Net Worth: $35,415

Losses in the share market reduced my net worth this month, as did a $1000 car engine repair bill. My Hesta fund seems to always have a constant balance, which is suspicious.

In spite of the losses, I made an income of approximately $2000 this month, so my overall net worth has only dropped a bit.

Kiva: $566

Vanguard Mutual Fund: $24442

Hesta Super Fund: $3336

Woodside Petroleum Shares: $1057

Car: $5825

Net Worth: $35,415

Losses in the share market reduced my net worth this month, as did a $1000 car engine repair bill. My Hesta fund seems to always have a constant balance, which is suspicious.

In spite of the losses, I made an income of approximately $2000 this month, so my overall net worth has only dropped a bit.

Subscribe to:

Posts (Atom)