The economic crisis has hit Melbourne's property markets. The government has tried to hold up property prices by increasing the First Home Buyer's Grant (FHBG). A first-home buyer can get around $20,000 or so for buying his first home. Many sellers have increased the price of their homes as an attempt to cash in. First home buyers tend to look for cheaper homes. It is unlikely that a first-home buyer will buy a $2 million Toorak mansion. Because of this, it is no surprise then that in the six months to September 2008, house prices in Toorak have fallen 24 per cent while house prices in Melton, a working-class suburb, have increased by 6 per cent in the same time period (read House Prices Fall in Top Suburbs).

Is this an opportunity to buy? I have a friend, a recent university graduate who is an engineer now, who believes that house prices in Melbourne are still overvalued. He is waiting for house prices to fall even further till he starts buying.

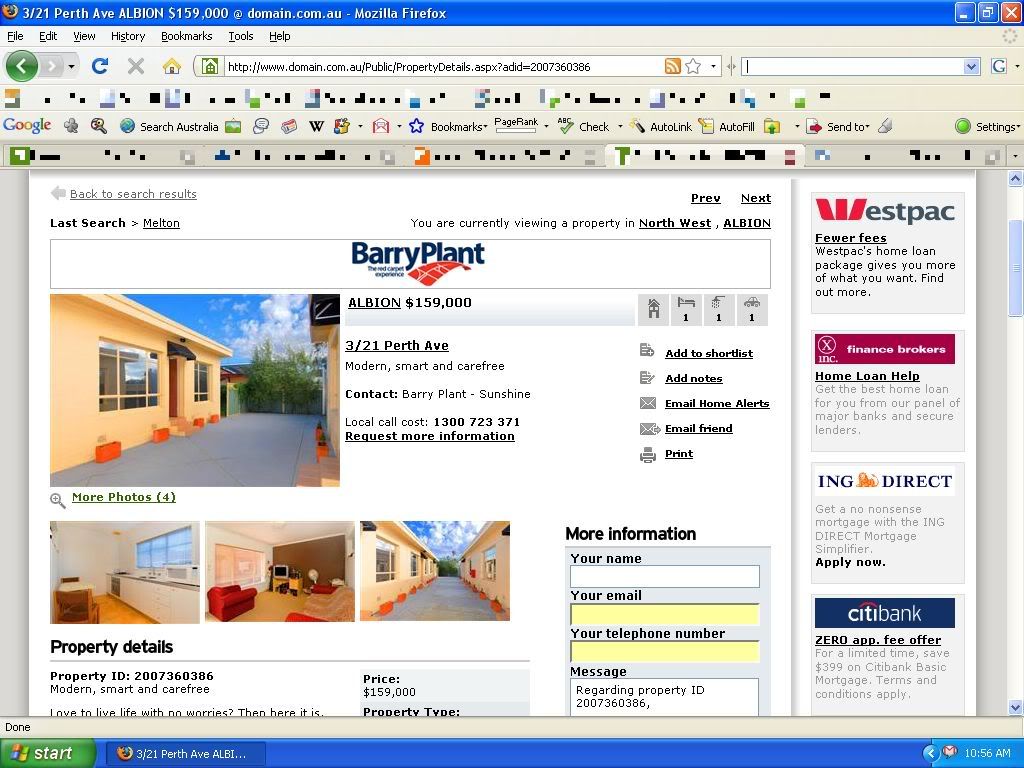

I went to Domain and do a search for houses in Melbourne. I tried to look for the cheapest house to buy and the cheapest house to rent. The cheapest house to buy in Melbourne that was listed when I checked was a unit in Albion for $159,000. The site claimed that a typical 25-year loan would see you pay $918 per month on mortgage repayments.

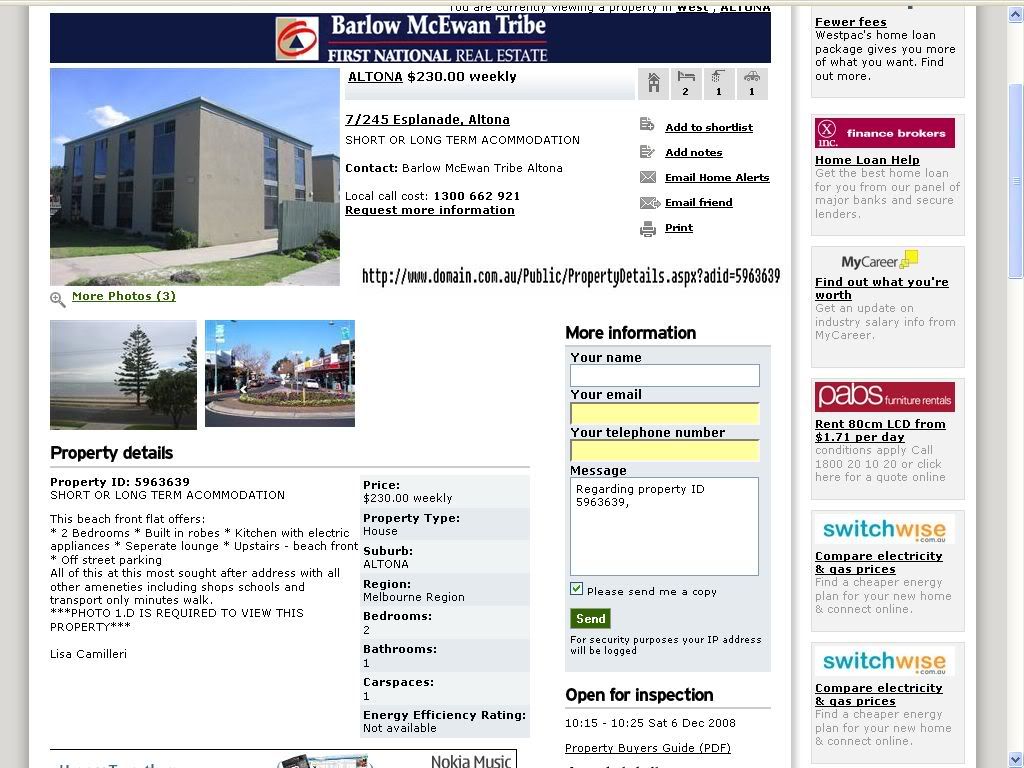

What about the cheapest place in Melbourne to rent? Based on my search, I found a unit in Altona for $170 a week. Both these places are very similar. They are both simple units in the Western suburbs of Melbourne. Paying $170 per week is equivalent to paying $680 per month.

Renting is cheaper in this case.

Remember you pay $918 a month if you buy a house. Paying $918 a month is equivalent to paying $230 a week. For $230 a week you can rent much nicer houses, for example this 2-bedroom seaside house in Altona. Based on casual observation of house and rent prices in Melbourne, it seems as if renting is cheaper than buying.

For someone who needs a home to live, they either have to take out a mortgage or rent a house. I currently live with my parents, so I have the freedom to save up first before I buy or rent a house. By buying a house without a loan, I am able to avoid interest, which can be quite substantial for 20-year loans. Some people claim that saving up will take too long. Suppose the house you want is $159,000 and the average salary is about $50,000. Assume you can save $40,000 of that, which would be fairly easy if you live with your parents. This means you should be able to save up for this house in about 3 or 4 years. That's not difficult.

One of the risks of buying houses that scares me is the fear of buying a house at a peak. For example, in Toorak the median house price is about $2,000,000. House prices in Toorak in the six months to September 2008 has gone down by 24 per cent, as I have stated earlier. This means that average house prices there went down $480,000! I would not feel good buying at a peak and then having my net worth drop by so much. Of course, if you buy cheap houses that problem is not so severe.

One solution to this problem is to diversify. Instead of buying one house with $159,000, put that money instead into a mutual fund that invests in various income-producing assets like property, bonds, and shares. Then simply use the income generated from this mutual fund to rent a house. Because your money is spread around so many different investments, risk is spread out. Furthermore, because you are renting, you have the freedom to move, which comes in handy if suddenly a child rapist moves next door or if a freeway or nuclear reactor is being built right next to your home. The income from this mutual fund will probably vary from time to time, so it is better to have to more money than $159,000 invested.

I predict that I will need about $200,000 invested to produce income that will allow me to rent a unit in a Western suburb. I will need $50,000 to produce income that will allow me to eat on about $3 a day. So all up I need a minimum of $250,000.

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment