You hear the words "economics" and "finance" often used interchangeably. There are, in fact, important differences between the two.

Economics is the study of markets. Markets are places where participants come and trade goods and services.

Finance, on the other hand, is the study of the financial market. The financial market is a market where borrowers and lenders meet. Borrowers are people who need money straight away, e.g. to start their own business. They do they by taking out loans or raising money by issuing shares. When borrowers take out loans or issue shares, there must be lenders or stockholders on the other side of the trade. These people lend money or buy stock. Finance is simply a study of the market where the patient (lenders) and the impatient (borrowers) meet.

It is clear from this that finance then is a branch of economics just like neuroscience is a branch of medicine. Buying and selling stocks or bonds is a finance issue whereas buying and selling oil is an economic issue. Economics is broader than finance because economics studies all markets whereas finance only studies financial markets.

All finance is economics but not all economics is finance.

22 December 2008

Similarities Between Economics and Medicine

What is economics? Adam Smith defined it as "the science of wealth." Lionel Robbins defines economics as the study of the "allocation and distribution of resources." There are many definitions, but when I think about economics I think about trade. Economics is the study of markets. Markets are places where trade takes place. Markets needn't be actual physical areas, e.g. Ebay is a market that exists on the Internet. Like a human body, markets can be healthy and unhealthy, and an economist's job is to analyze the market, make measurements, make forecasts, treat any sicknesses, and so on.

Economics then is very similar to medicine. The difference is that economists study markets while physicians study the human body. While physicians measure blood pressure, blood glucose, cholesterol levels, etc, economists measure interest rates, inflation, etc. Within medicine there are different schools of thought, e.g. allopathic medicine versus osteopathic medicine. Economics has different schools of thought as well, e.g. monetarism and Keynesianism.

Economics and medicine also share ambiguity. Because the two disciplines study complex systems, there are many unknowns. In medicine, nobody knows how drinking coffee seems to reduce the likelihood of getting Parkinson's disease. In economics, nobody really knows why or how business cycles form and what to do with them.

Economics then is very similar to medicine. The difference is that economists study markets while physicians study the human body. While physicians measure blood pressure, blood glucose, cholesterol levels, etc, economists measure interest rates, inflation, etc. Within medicine there are different schools of thought, e.g. allopathic medicine versus osteopathic medicine. Economics has different schools of thought as well, e.g. monetarism and Keynesianism.

Economics and medicine also share ambiguity. Because the two disciplines study complex systems, there are many unknowns. In medicine, nobody knows how drinking coffee seems to reduce the likelihood of getting Parkinson's disease. In economics, nobody really knows why or how business cycles form and what to do with them.

16 December 2008

To Alarm or Not to Alarm?

If I go to bed and sleep normally, I usually get a little more than 8 hours of sleep. I once thought that this was okay because many people told me that you should get "at least eight hours of sleep."

According to WebMD, if I get over 8 hours of sleep per night, the risks of getting type 2 diabetes increases significantly: "A study in Diabetes Care shows men who got little sleep (up to five or six nightly hours) or a lot of sleep (more than eight hours per night) were more likely to develop diabetes than men with moderate amounts of nightly sleep."

Source: http://www.medscape.com/viewarticle/527652

I adjusted my lifestyle according once I read this. I use an alarm clock to wake me up 7.5 hours after I go to bed, ensuring that I do not get more than 8 hours of sleep.

However, I few weeks later I read a UK Daily Mail news article that claims that waking up to an alarm clock is bad for you because it can raise your blood pressure and lead to hypertension. Hypertension can lead to heart attack, stroke, or kidney failure.

"In a study conducted by the National Institute of Industrial Health in Japan, participants who were suddenly forced awake had higher blood pressure and heart rate than those allowed to wake up in their own time.

"Dr Chris Idzikowski of the Edinburgh Sleep Centre explains that subtle body changes that occur during sleep make us vulnerable in the early hours - and an alarm sounding only exacerbates this.

"During the later part of night, the body's general physiology is less well regulated. This means the fluctuations in blood pressure, heart rate and breathing are more extreme than usual. Also because you are lying relatively still, blood thickens up a bit more, with a degree of blood clotting."

Source: http://www.dailymail.co.uk/health/article-412283/How-alarming-Your-bedside-clock-bad-health.html

So I face a dilemma. Either I set my alarm every night and face high blood pressure, which leads to cardiovascular disease or I do not set the alarm every night, oversleep, get diabetes, which can also leads to cardiovascular disease. So either way it seems as if I get cardiovascular disease anyway.

What can I do to resolve this dilemma?

According to WebMD, if I get over 8 hours of sleep per night, the risks of getting type 2 diabetes increases significantly: "A study in Diabetes Care shows men who got little sleep (up to five or six nightly hours) or a lot of sleep (more than eight hours per night) were more likely to develop diabetes than men with moderate amounts of nightly sleep."

Source: http://www.medscape.com/viewarticle/527652

I adjusted my lifestyle according once I read this. I use an alarm clock to wake me up 7.5 hours after I go to bed, ensuring that I do not get more than 8 hours of sleep.

However, I few weeks later I read a UK Daily Mail news article that claims that waking up to an alarm clock is bad for you because it can raise your blood pressure and lead to hypertension. Hypertension can lead to heart attack, stroke, or kidney failure.

"In a study conducted by the National Institute of Industrial Health in Japan, participants who were suddenly forced awake had higher blood pressure and heart rate than those allowed to wake up in their own time.

"Dr Chris Idzikowski of the Edinburgh Sleep Centre explains that subtle body changes that occur during sleep make us vulnerable in the early hours - and an alarm sounding only exacerbates this.

"During the later part of night, the body's general physiology is less well regulated. This means the fluctuations in blood pressure, heart rate and breathing are more extreme than usual. Also because you are lying relatively still, blood thickens up a bit more, with a degree of blood clotting."

Source: http://www.dailymail.co.uk/health/article-412283/How-alarming-Your-bedside-clock-bad-health.html

So I face a dilemma. Either I set my alarm every night and face high blood pressure, which leads to cardiovascular disease or I do not set the alarm every night, oversleep, get diabetes, which can also leads to cardiovascular disease. So either way it seems as if I get cardiovascular disease anyway.

What can I do to resolve this dilemma?

09 December 2008

Lying to Children about Santa Claus

At work the other day a co-worker told me that she told her son the truth about Santa Claus and the boy, who was almost a teenager, was devastated. The son cried for a long time and accused his parents of cruelty. When the son asked why the mother did this to him, the mother said, "When you have kids, you'd do the same."

I asked this mother why she lied to her child like this and she said, "We're Christians, so it's part of our tradition to celebrate Christmas."

This doesn't make any sense to me. Look at what the Bible says:

If the Bible claims that lies are an abomination to the Lord, then why would a Christian knowingly lie to his or her child about Santa Claus? And what does Santa Claus have to do with Christianity? There is no mention of Santa Claus, flying reindeer, or Christmas trees in the Bible.

I asked this mother why she lied to her child like this and she said, "We're Christians, so it's part of our tradition to celebrate Christmas."

This doesn't make any sense to me. Look at what the Bible says:

Lying lips are an abomination to the Lord.

-Proverbs 12:22

If the Bible claims that lies are an abomination to the Lord, then why would a Christian knowingly lie to his or her child about Santa Claus? And what does Santa Claus have to do with Christianity? There is no mention of Santa Claus, flying reindeer, or Christmas trees in the Bible.

Buy or Rent in Melbourne?

The economic crisis has hit Melbourne's property markets. The government has tried to hold up property prices by increasing the First Home Buyer's Grant (FHBG). A first-home buyer can get around $20,000 or so for buying his first home. Many sellers have increased the price of their homes as an attempt to cash in. First home buyers tend to look for cheaper homes. It is unlikely that a first-home buyer will buy a $2 million Toorak mansion. Because of this, it is no surprise then that in the six months to September 2008, house prices in Toorak have fallen 24 per cent while house prices in Melton, a working-class suburb, have increased by 6 per cent in the same time period (read House Prices Fall in Top Suburbs).

Is this an opportunity to buy? I have a friend, a recent university graduate who is an engineer now, who believes that house prices in Melbourne are still overvalued. He is waiting for house prices to fall even further till he starts buying.

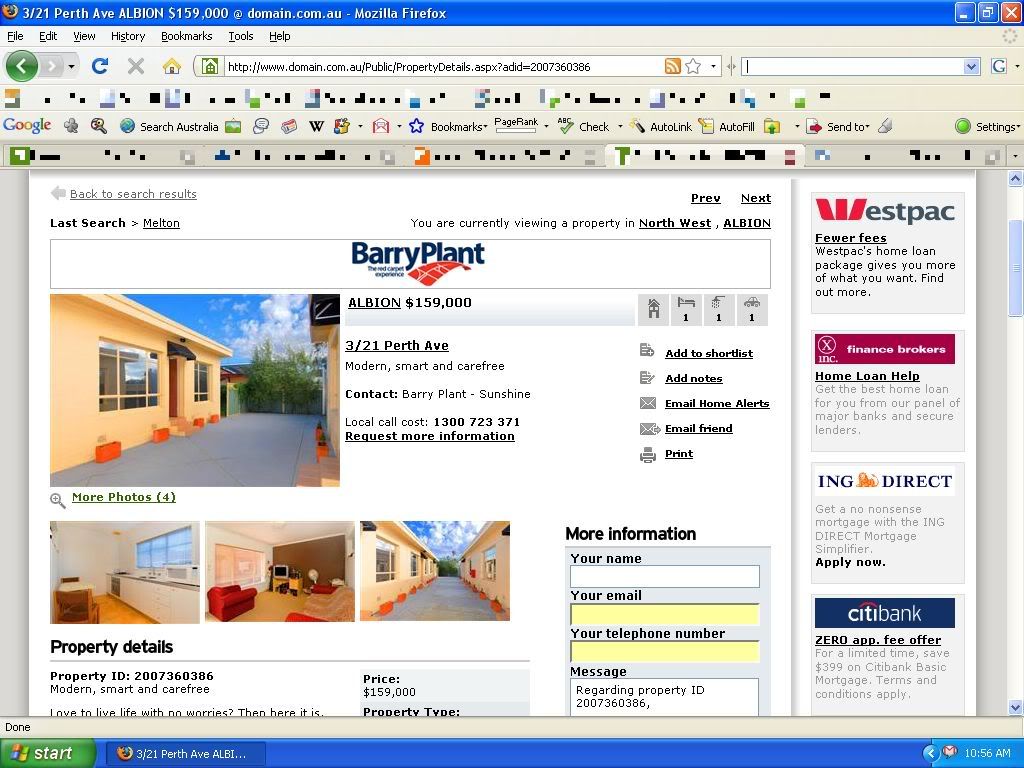

I went to Domain and do a search for houses in Melbourne. I tried to look for the cheapest house to buy and the cheapest house to rent. The cheapest house to buy in Melbourne that was listed when I checked was a unit in Albion for $159,000. The site claimed that a typical 25-year loan would see you pay $918 per month on mortgage repayments.

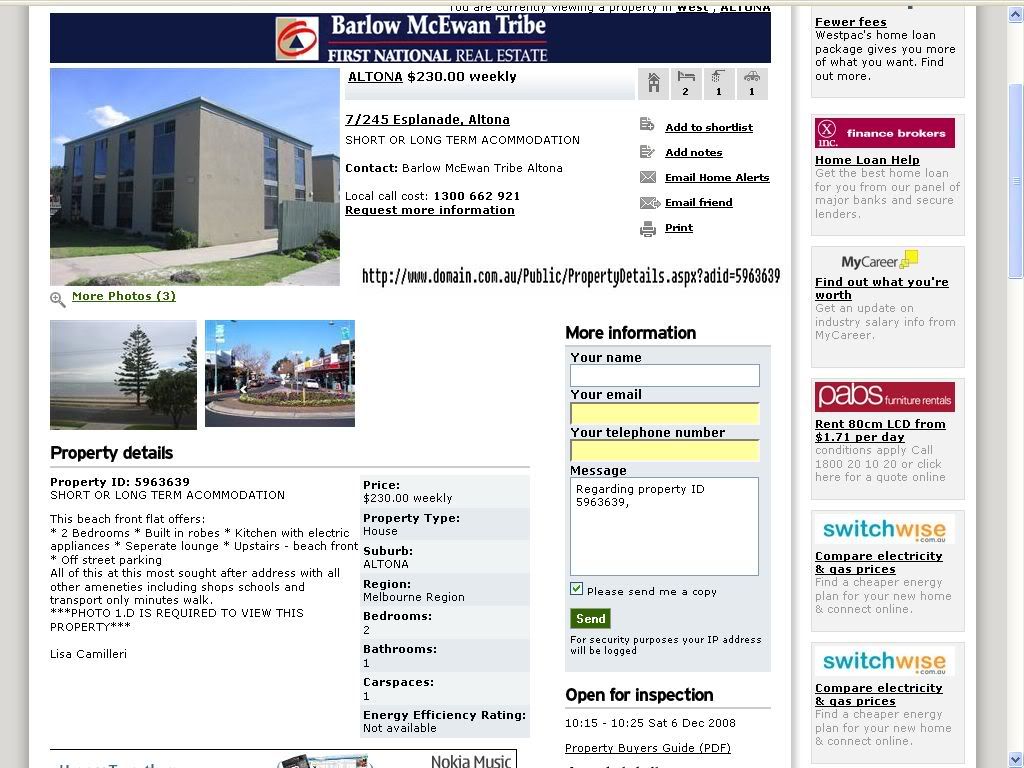

What about the cheapest place in Melbourne to rent? Based on my search, I found a unit in Altona for $170 a week. Both these places are very similar. They are both simple units in the Western suburbs of Melbourne. Paying $170 per week is equivalent to paying $680 per month.

Renting is cheaper in this case.

Remember you pay $918 a month if you buy a house. Paying $918 a month is equivalent to paying $230 a week. For $230 a week you can rent much nicer houses, for example this 2-bedroom seaside house in Altona. Based on casual observation of house and rent prices in Melbourne, it seems as if renting is cheaper than buying.

For someone who needs a home to live, they either have to take out a mortgage or rent a house. I currently live with my parents, so I have the freedom to save up first before I buy or rent a house. By buying a house without a loan, I am able to avoid interest, which can be quite substantial for 20-year loans. Some people claim that saving up will take too long. Suppose the house you want is $159,000 and the average salary is about $50,000. Assume you can save $40,000 of that, which would be fairly easy if you live with your parents. This means you should be able to save up for this house in about 3 or 4 years. That's not difficult.

One of the risks of buying houses that scares me is the fear of buying a house at a peak. For example, in Toorak the median house price is about $2,000,000. House prices in Toorak in the six months to September 2008 has gone down by 24 per cent, as I have stated earlier. This means that average house prices there went down $480,000! I would not feel good buying at a peak and then having my net worth drop by so much. Of course, if you buy cheap houses that problem is not so severe.

One solution to this problem is to diversify. Instead of buying one house with $159,000, put that money instead into a mutual fund that invests in various income-producing assets like property, bonds, and shares. Then simply use the income generated from this mutual fund to rent a house. Because your money is spread around so many different investments, risk is spread out. Furthermore, because you are renting, you have the freedom to move, which comes in handy if suddenly a child rapist moves next door or if a freeway or nuclear reactor is being built right next to your home. The income from this mutual fund will probably vary from time to time, so it is better to have to more money than $159,000 invested.

I predict that I will need about $200,000 invested to produce income that will allow me to rent a unit in a Western suburb. I will need $50,000 to produce income that will allow me to eat on about $3 a day. So all up I need a minimum of $250,000.

Is this an opportunity to buy? I have a friend, a recent university graduate who is an engineer now, who believes that house prices in Melbourne are still overvalued. He is waiting for house prices to fall even further till he starts buying.

I went to Domain and do a search for houses in Melbourne. I tried to look for the cheapest house to buy and the cheapest house to rent. The cheapest house to buy in Melbourne that was listed when I checked was a unit in Albion for $159,000. The site claimed that a typical 25-year loan would see you pay $918 per month on mortgage repayments.

{kind=link}

What about the cheapest place in Melbourne to rent? Based on my search, I found a unit in Altona for $170 a week. Both these places are very similar. They are both simple units in the Western suburbs of Melbourne. Paying $170 per week is equivalent to paying $680 per month.

{kind=link}

Renting is cheaper in this case.

Remember you pay $918 a month if you buy a house. Paying $918 a month is equivalent to paying $230 a week. For $230 a week you can rent much nicer houses, for example this 2-bedroom seaside house in Altona. Based on casual observation of house and rent prices in Melbourne, it seems as if renting is cheaper than buying.

{kind=link}

For someone who needs a home to live, they either have to take out a mortgage or rent a house. I currently live with my parents, so I have the freedom to save up first before I buy or rent a house. By buying a house without a loan, I am able to avoid interest, which can be quite substantial for 20-year loans. Some people claim that saving up will take too long. Suppose the house you want is $159,000 and the average salary is about $50,000. Assume you can save $40,000 of that, which would be fairly easy if you live with your parents. This means you should be able to save up for this house in about 3 or 4 years. That's not difficult.

One of the risks of buying houses that scares me is the fear of buying a house at a peak. For example, in Toorak the median house price is about $2,000,000. House prices in Toorak in the six months to September 2008 has gone down by 24 per cent, as I have stated earlier. This means that average house prices there went down $480,000! I would not feel good buying at a peak and then having my net worth drop by so much. Of course, if you buy cheap houses that problem is not so severe.

One solution to this problem is to diversify. Instead of buying one house with $159,000, put that money instead into a mutual fund that invests in various income-producing assets like property, bonds, and shares. Then simply use the income generated from this mutual fund to rent a house. Because your money is spread around so many different investments, risk is spread out. Furthermore, because you are renting, you have the freedom to move, which comes in handy if suddenly a child rapist moves next door or if a freeway or nuclear reactor is being built right next to your home. The income from this mutual fund will probably vary from time to time, so it is better to have to more money than $159,000 invested.

I predict that I will need about $200,000 invested to produce income that will allow me to rent a unit in a Western suburb. I will need $50,000 to produce income that will allow me to eat on about $3 a day. So all up I need a minimum of $250,000.

Subscribe to:

Posts (Atom)